The covid-19 pandemic has shown the entire world that nothing is certain and you might face emergencies indeed. You may get laid off from your permanent job, you may come across sudden serious illness or even death. Your businesses may get shut down. Your investments may also go into depreciation for a year or so. In such a critical situation you will be the only one who can help yourself.

You might have observed in your life that when difficulties come if you are financially secured, you are mentally stable and confident to face that extreme situation. On the contrary, If you are not financially secure, you will become more stressed and end up losing control over the situation. In such a situation, the emergency fund is your friend.

By now the pandemic taught us that emergency funds are so important, but still many of us do not own them.

Table of Contents

What might be the reasons for it?

- We don’t know how much security money is required and where to park it.

- We always think that this month we don’t have that much money so we will do it later.

- We lack disciplined ways of investment.

- We think right now we have lots of more important financial goals like classy gadgets, Child education, a new car, a new home, etc.

- We think we will manage money from parents, friends, and relatives. What’s the big deal?

- And lastly, We are not keen enough to learn about personal finance.

If all these are your reasons, this article is for you. This will make you understand how important and simple having an emergency fund is if you take small steps.

In this blog, we will learn the following things.

- What is an emergency fund?

- How much emergency fund you should have?

- How to build an emergency fund?

- Tips for starting an emergency fund

- Best practices to maintain your emergency fund

- Conclusion.

What is an emergency fund?

An emergency fund is nothing but a fund that you deliberately park aside separately from your regular savings or investments. This fund can be utilized in case you face any kind of emergency.

There will be a few emergency events like death, accidents or serious illness, etc. which might not be predictive in nature but still, you can safeguard yourself by taking insurance. E.g Health insurance, life insurance, etc. Hence Insurance is one of the types of emergency funds one should avail of first.

However, there will be a few emergencies which will be sudden events e.g sudden loss of job, recession, natural calamities like the Covid-19 pandemic, etc. wherein you lose your regular monthly income however your monthly expenses will still be there. As you can not predict these events, you have to be prepared financially for such a situation so that you can survive for that particular period.

There are few businesses which are also having fluctuating monthly incomes, in such cases also having emergency funds play a vital role.

How much emergency fund you should have?

The finance experts all over the world say that an emergency fund shall be at least 6 months of your monthly expense. Once you reach this goal, you shall increase it to 12 months of your monthly expense. You may also feel that 6 months’ expenses are enough, however in case you actually had an emergency and you used this fund completely, then you are again back to zero and hence 12 months emergency fund is an ideal fund size.

You surely going to struggle a lot to park aside this much money as if you are in your twenties, you might not have much income. And if you are a married person in your thirties, you might have a lot of liabilities. But trust me, friends, you have to prioritize your emergency fund over your savings and investments.

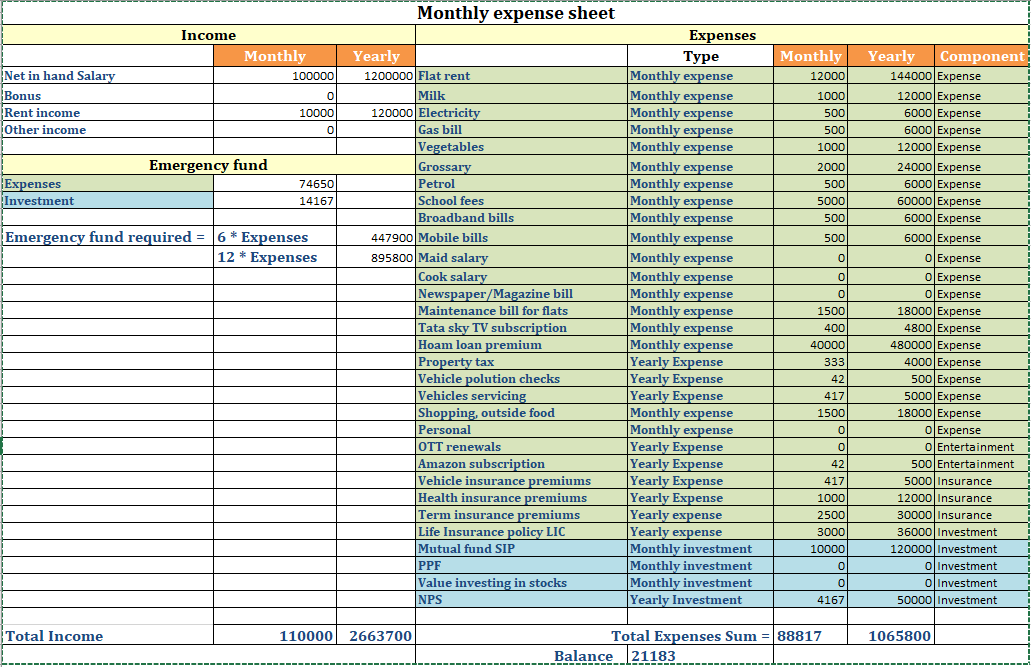

Now as we say an emergency fund is a multiple of monthly expenses, let me tell you what exact monthly expense you should consider.

Below is a sample monthly expense calculation summary I have listed for ready reference. This is just an illustrative example so you can modify it as per your needs.

Here as you can see the monthly expense excluding your investments shall be considered as your pay bills for which you must have an emergency fund with you. You may also observe that here in this exhaustive list I have only considered the needs but not the wishes. You might be having a party every month or you might be a shopping lover, but you will obviously not be bothered about it when you have no salary. So such luxuries are not to be considered unnecessary in your monthly expense calculation.

You shall make some efforts and make this sheet for your case to derive the emergency fund value. This might be an eye-opener for you to get a sense of how much % of your money you spend monthly.

How to build an emergency fund?

Now you know the target figure to which you need to reach. You may feel, in the above example, that accumulating 4.47 lakhs or 8.95 lakhs will take at least 1-2 years. But this is the fact and you can’t deny it. The only thing you can do is to accumulate it as early as possible. Even if it takes time, still something is always better than nothing.

Now where to keep this emergency fund? Just simply keeping all the money in cash or in the bank will not beat inflation.

Ideally, you can have the following bifurcation.

- 5% in cash: This is to serve you instant help.

- 15% in saving bank: Even if the saving bank may not beat inflation, still here what is more important is you shall be able to withdraw some money from an ATM.

- 80% in Liquid mutual funds. Liquid funds are best because you can withdraw on the same day. You do not have an exit load or any extra penalty for breaking funds and it can at least beat the inflation rate.

- On top of that, if still you face some challenges to withdraw liquid funds, this is the time you should swap your Credit card.

You can always choose a cash and savings fund % suitable to your total emergency fund. However, it is highly recommended to keep at least 70% in Liquid Funds.

Tips for starting an emergency fund

- Cut down your luxury expenses for a year. This might not help greatly but that’s the least you can do.

- In the above example, as you can see, you still have some extra 20K money which you might either spend or invest somewhere e.g in MF. Prioritize your emergency fund over your investment. This is because when you have an emergency and you don’t have funds any way you will break those investments. Hence stop investments for a year and start a liquid fund where the capital is secured at low risk and your money will be growing at a rate minimum equal to inflation.

- If ever you get any lump sum money like your FD maturity, company bonus, or Diwali bonus, directly park this money in an emergency fund.

- Adopt a disciplined way. It means start SIP in such a way that as soon as you get your salary on the 1st of the month, the next day some X amount is auto deducted to some liquid MF directly.

This works like a wonder. Many times we do not take action just because of our laziness. Hence automate your investments.

Read this also:-9 Top Highly-Paid Freelance Jobs Start in 2022!

Best practices to maintain your emergency funds.

- Have a separate Saving bank account for parking your emergency fund to which you don’t have easy withdrawal access. No net banking or UPI linked. No Debit card handy.

- Give some part of the money to your parents. Once given to them, you will obviously hesitate to take it back.

- Treat emergency funds as security and not as an investment. Hence do not park your emergency fund in risky and volatile assets like the stock market, cryptocurrency, or gold.

- Emergency funds shall have liquidity. It means when you need it, it shall be available to you within a few hours. Hence do not park your emergency fund in assets like real estate or PPF etc.

- Review your expenses and emergency fund quarterly.

Conclusion:

You only need four things to start an Emergency Fund.

- Emergency funds are a need and not an investment. E.g Set a goal ( 6 x of monthly expense).

- Prepare a plan (5-15-80).

- Parking your fund in a separate bank from where money will get deducted to liquid funds automatically.

- Stick to it until the goal is reached and live stress-free.